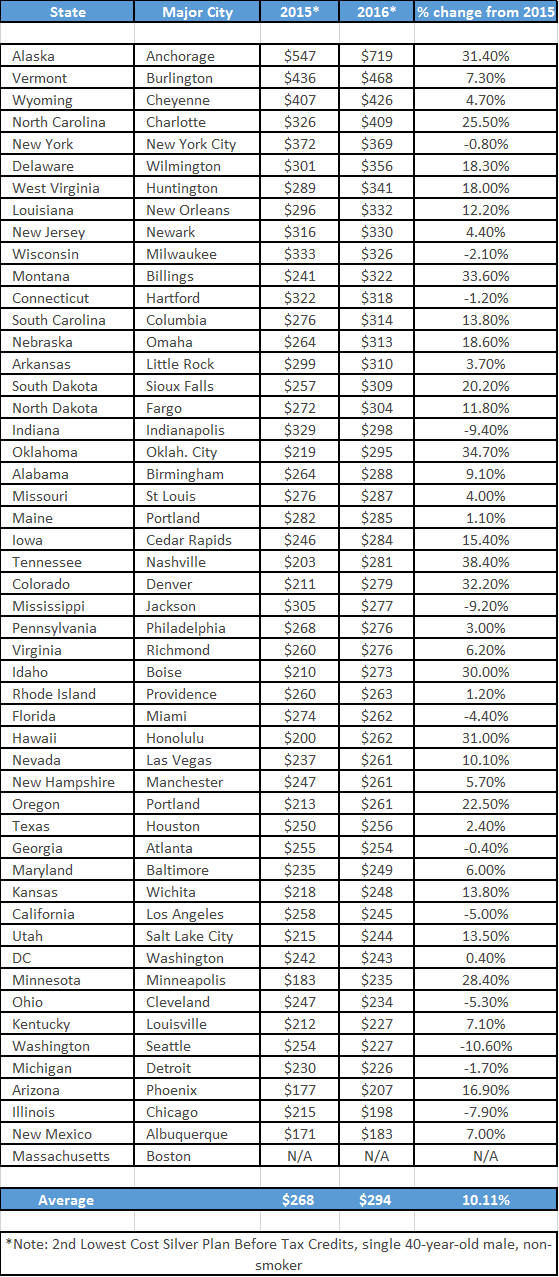

Health insurance costs by state and Provider Fees

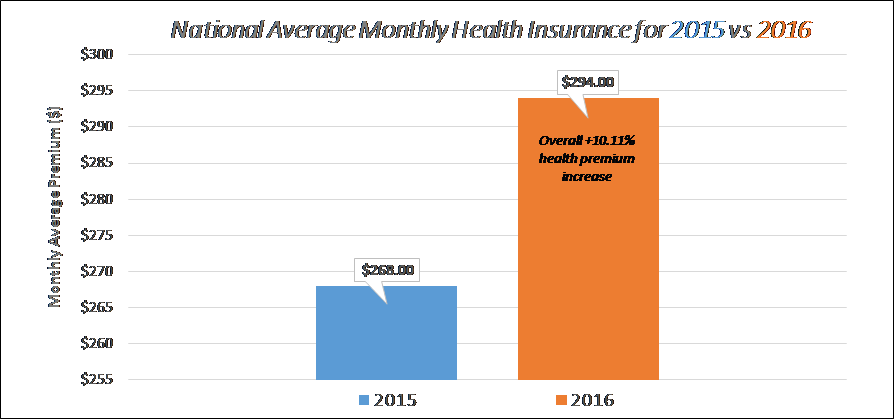

Health insurance costs are up for 2016. Monthly premium for most popular plans offered on/off the marketplace exchanges in 2016 are 10.11% higher on average than they were in 2015, according to the Kaiser Family Foundation reported on October 27th 2015 when final rates were filed for the 2016 plan year.

Comparing monthly premiums, deductibles and copays based on a single, 40-year-old, non-smoking male, the study highlighted ALL states based on health insurance premium for the 2nd lowest cost silver plan, before tax credits.

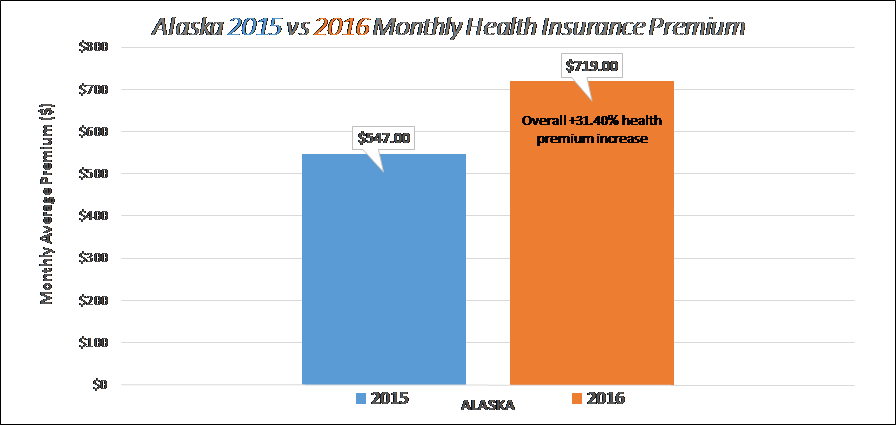

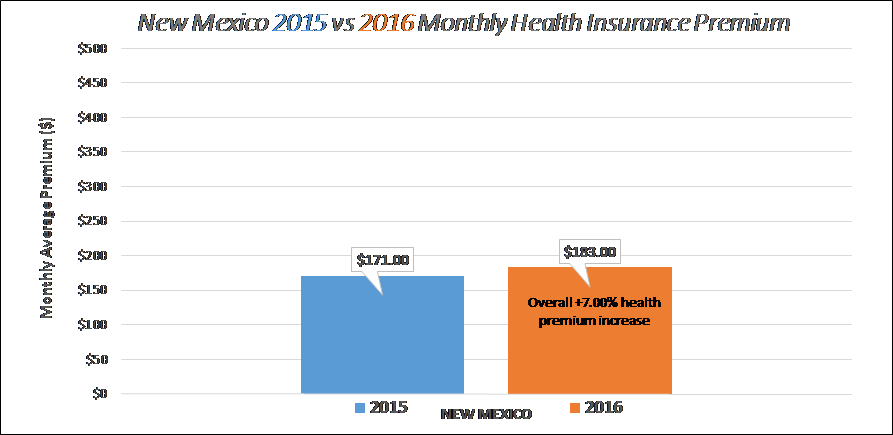

If you live in one of these states that are at a higher cost, you should expect to pay more each month for your insurance. Unfortunately, you’ll also be paying more for each doctor or emergency room visit, as the highest costs plans charge higher co-insurance rates, copays and reimbursement rates to providers. Starting with the number 1 state, Alaska with an average monthly premium of $719 and ending with New Mexico at $183.00 month for a silver plan (actuarial value of 70%) in 2016.

Arizona ranked 46th lowest cost plan out of 50 states at $207.00 per month with an average increase of 16% in 2016. Still below the national average of $294.00 per month but above the naltional inflation of health insurance of 10.11% increase. – What does this mean? Arizona is growing at a faster rate than the national average. 6% higher trend than the nation as a whole for a similar (2nd lowest silver) plan. Three factors are measured to gauge healthcare costs and trends, with all three being interrelated:

- Total HealthCare Spend including prescription drugs

- Utilization

- Cost of providing health insurance

- New Goverment mandates, treatments, technology, and therapies

- Rise in fees charged for medical care and services

- Price Inflation

The study titled “Will physician Unions Improve Health System Proformance“ shows physician collective bargaining has historically focused on physician compensation and not on patient care issues. Some would say consolidation of providers would improve economic effciency, quality and costs. Evidence demostrates the exact opposite, physician collective bargaining is unlikely to improve the quality of that care consumers receive or lower prices for healthcare services. Provider consolidation gives hospitals greater negotiating strength and limits competition, resulting in higher prices for services, patients, and no improvmnent in quality of care. On the chart above, I would coorelate the inverse link with higher the percentage increase, the less competition among providers. The Journal of Law & Economics studied of the relationship between competition and hospital prices and they have found that hospital concentration is associated with increased prices, regardless of whether the hospitals is for-profit or non-profit. All medical care is local. Once a single system is able to lock up the delivery of most of a region’s medical care, continued price hikes will be inescapable.

In a nutshell: Premiums follow costs. With more consolidation of healthcare delivery, where doctors and hospitals are merging at record pace, less competition is tranforming the medical marketplace into a land of giants. According to the American Health Insurance Plans, last year a 15 minute visit to the doctor in private practice costs $69…The same visit to a hospital-employed physician costs $245.

How are reimbursements to providers measured and determined? Three methods of payments are typically used between the insurance carriers and hospitals which ultimately affects your monthly premiums:

- Case-Based Payments or Distinct Diagnostically Related Cases (D.R.G.’s)

- A set amount of dollars per day or called Per-Diem payments

- Fees-for-service payments or schedule of copays

The first method, Care-Based Payemnts or Distinct Dianostically Related Cases (D.R.G.’s) are used by federal and state medical plans, such as Medicare and Medicaid. The D.R.G method of some 750 diagnosis codes is a benchmark in which the other two methods are priced. Some critics of the federal Medicare program routinely call Medicare a “dumb” benchmark for prices/fees. Perhaps it is, but no one really understands the determinants of the wide variations among fees paid to hospitals for basically the same medical episode. The per-diem and fee-for-service methods are predominantly used by private insurers with these reimbursement fees exceeding the hospital’s cost of providing the underlying services. The profit built into these larger payments cover the losses hospitals book on servicing Medicare and Medicaid patients under the D.R.G. payment model. Presumably, the larger the insurance company with more market-power, the lower the fees to providers and shared responsibility for members. Vis-à-vis happens with smaller carriers that do not have the marketshare to drive down the fees. Notice the provider offices/hospitals (Honor Health/John C Lincoln) and insurance companies (Aetna/Humana) are merging at a record pace? This is an attempt for the providers to have a higher reimbursement rates while the insurance companies try to leverage market-power of its member population to control costs.

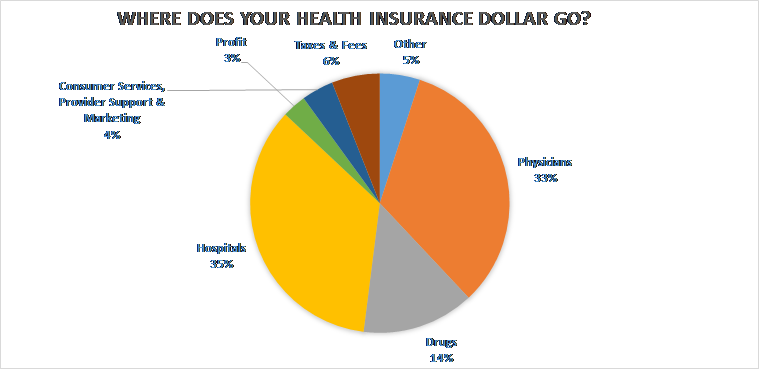

Where does the money go?

TREK FACT: Due to ACA laws for fully insured-plans, insurance carriers MUST pay $.80/$.85 for every $1.00 they collect, so 80% (< 50 employees, includes individual policies) or 85% (> 50 employees) of your premium you pay each month is going toward claims, known as “medical loss ratio.”

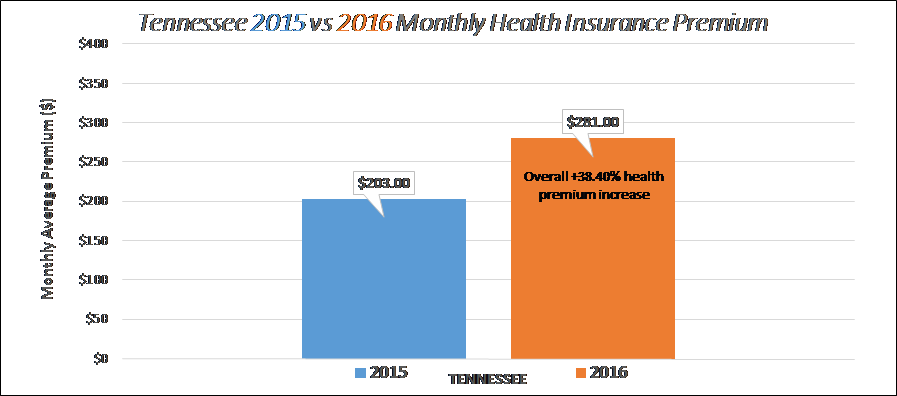

Largest Increase for 2016 (38.4%): Tennessee

Largest Monthly Rates for 2016 ($719.00): Alaska

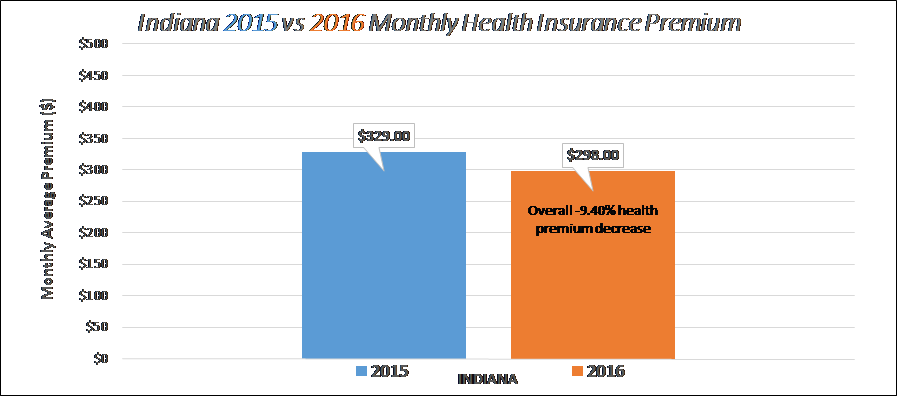

Lowest Decrease for 2016 (-9.40%): Indiana

Lowest Monthly Rate for 2016 ($183.00): New Mexico

National Average for 2016 ($294.00 at +10.11%):