Intro to alternative funding options

Intro to alternative funding options:

As employee healthcare benefit costs continue to consume a greater share of the bottom line, many organizations are finding an alternative to the traditional fully insured model for businesses, known as level-funded or self-funded options.

While traditional fully insured plans, backed by a commercial insurance company, offer the security of a known monthly expenditure, many employers complain about the rigidity of plan design, lack of cost containment and underperformed or weak customer service. Many of these issues can be addressed through a level/self-insured plan, in which the employer takes on more financial risk of its enrollees’ healthcare.

Some products such as “level-funding” are built to provide a step in the direction of self-funding for small groups (> 100 employees) for the potential surplus in claim savings. Level funding provides all advantages as self-funding but adds predictability on costs much like a traditional fully insured policy.

Level-funding advantages

- Pre-set monthly payments

- Total cost is comprised of claims funding and administration costs. Payments do not fluctuate based upon claims experience.

- Monthly detailed reporting

- Know exactly how your healthcare dollars are being spent.

- Highlight utilization trends in spending (such as overuse of emergency services), so you can offer education and identify opportunities for savings.

- Help to take an active role in plan administration by making adjustments where needed.

- Savings Potential

- When claims are less than expected, the company and employees benefit by receiving claims savings in the form of premium credit, which in turn lowers your monthly premiums.

- Flexibility in plan design

- You choose the plan that fits your employees’ needs. You have the ability to change your plan based on the data in the monthly reporting.

- Large claim protection

- Included in the administration costs, insurance is purchased for unexpected large claims known as specific/individual stop loss protection as well as an aggregate stop loss protection. These stop loss limits are based and calculated on a verity of factors.

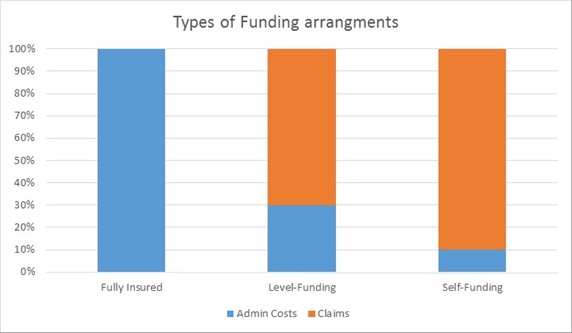

The below chart is the different types of funding arrangements an employer can select. Typically, the larger the company, the more “creditable” the group becomes in predicting claims from a health insurance actuary. The orange section is the potential claims savings.

Self/level-funding can provide an excellent vehicle to navigate the future of healthcare and benefits. The flexibility it affords, combined with the responsibility for plan expenses, produces an incentive for employers to both reduce healthcare costs and offer the benefits that are best suited to their employee population. While it’s not necessarily the best solution for every employer, you can benefit a great deal from learning more about your options and exploring what self/level-funding can do for you, your organization and your employees.

Hiring a well-qualified and trusted broker/consultant is crucial for a successful program. I have been working with clients on these types of alternative funding arrangements for over 10 years with plenty of experience and know-how. Contact me to find out more or generate a proposal your specific company with more than 25 eligible employees.